When a cyber incident brings your business operations to a halt, every minute counts. Lost sales, disrupted services, and unexpected recovery costs can add up fast. That’s why having cyber business interruption coverage is so important.

But there’s one detail that often gets overlooked — and it can make a big difference in how and when your coverage actually kicks in. It’s called the business interruption waiting period.

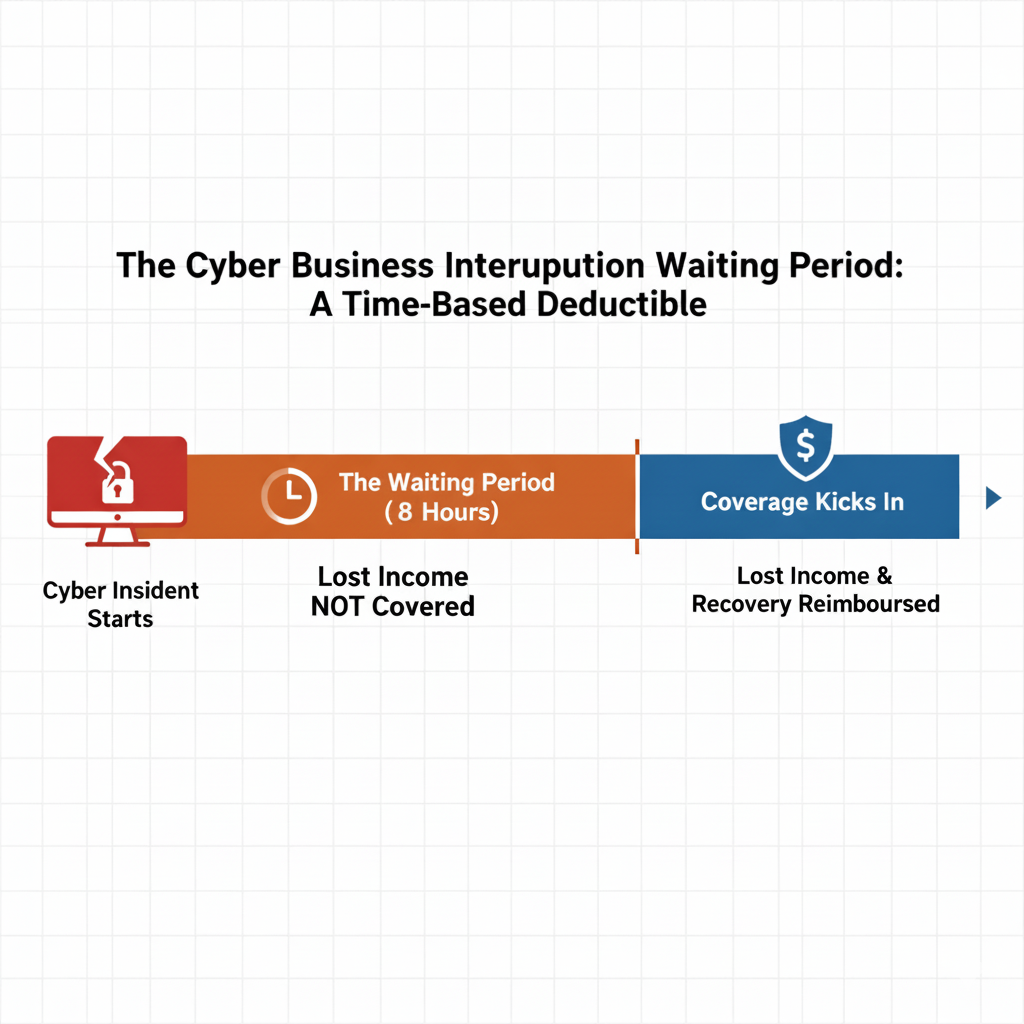

What Is a Business Interruption Waiting Period?

The waiting period in a cyber insurance policy is the amount of time that must pass after a covered cyber event before your business interruption coverage begins to reimburse you for lost income.

Think of it like a time-based deductible. Instead of paying out of pocket for a certain dollar amount, you’re responsible for losses that occur during the waiting period — typically measured in hours rather than days.

For example, if your policy includes a 8-hour waiting period, any income lost during the first 8 hours of a system outage or cyber incident isn’t covered. Once that time passes, coverage begins for the duration of the business interruption, up to your policy limits.

Common Waiting Periods

Every policy is different, but most cyber insurance policies set the waiting period between:

-

8 and 24 hours for small and midsize businesses

-

24 to 48 hours for larger organizations with more complex systems

A shorter waiting period means the policy will begin reimbursing you sooner — but it can also result in a slightly higher premium.

Why the Waiting Period Matters

Understanding your policy’s waiting period is crucial for setting expectations and planning your response strategy. Here’s why it’s important:

-

Helps You Plan for Short-Term Downtime

If your business can handle short outages without significant financial strain, a longer waiting period may be acceptable. But if even a few hours of downtime cause meaningful losses, you’ll want to consider a shorter one. -

Affects When Reimbursement Begins

Knowing your waiting period helps you forecast when coverage will start paying out, so you can better manage cash flow during an incident. -

Clarifies Coverage Gaps

Many businesses underestimate how quickly downtime costs add up. Understanding the waiting period ensures you know exactly how much loss you’re responsible for before coverage applies. -

Guides Risk Management Decisions

The waiting period is a reminder that prevention and preparedness still matter. Investing in backup systems, redundant networks, or incident response plans can help minimize downtime and reduce the impact of that uncovered period.

Example: How the Waiting Period Works

Let’s say your company experiences a ransomware attack that locks your systems for 36 hours. Your cyber policy includes a 12-hour waiting period.

-

The first 12 hours of lost income are not covered.

-

The next 24 hours of income loss and recovery expenses are covered under your business interruption section.

If your systems had been restored within 10 hours, the entire event would have fallen within the waiting period — meaning there would be no reimbursable loss under that portion of the policy.

The Bottom Line

Your cyber business interruption coverage is designed to help you recover financially when a cyber event shuts down your operations. But the waiting period determines when that support begins — and understanding it ensures there are no surprises when you need your coverage most.

At Redwood Insurance Agency, we help businesses understand the fine print in their cyber policies — from waiting periods to system failure coverage — so they can be confident their protection matches their real-world risks.

If you’re unsure how your cyber insurance would respond to an interruption, our team can help you review your current coverage and identify any gaps before a disruption happens.